A newsletter for modern marketers.

TRUSTED BY THE WORLD'S SMARTEST MARKETERS

Free ad performance benchmarks every week.

Live webinars and strategy sessions with industry leaders.

Watch all previous episodes on our YouTube channel.

Insider strategies from the smartest brands in ecommerce.

SEE LATEST POSTS:

February 2026 Data: How Enterprise Businesses Are Performing

February is our first clean look at how larger ecommerce businesses are carrying the 2025 story into 2026. The question is straightforward: are $50M–$100M and $100M+ businesses still buying growth on weaker unit economics, or are they starting to repair efficiency while they scale?

This piece focuses on two size bands:

- $50M–$100M in annual revenue

- $100M+ in annual revenue

All numbers cited are median year-over-year changes from Northbeam's February 2026 dataset.

Why These Size Bands Matter

In our 2025 review, most of the market-level topline expansion came from businesses above $50M in annual revenue. On a median basis:

- $50M–$100M increased ad spend by roughly 17.5% and revenue by 15.3%

- $100M+ increased spend about 22.9% and revenue about 15.2%

The pattern was consistent: as you move up the revenue ladder, you see more spend, more revenue, and higher first-time CAC. Larger businesses were willing to trade efficiency for market share.

February 2026 tells us whether that posture is still the right one, or whether the biggest players are finally converting scale into healthier economics.

February at a Glance: Large Businesses vs. the Market

Across all businesses, median performance in February 2026 looked like this, year over year:

- Spend: +10.40%

- Revenue: +9.56%

- New-customer revenue: –1.46%

- MER: +0.73%

- New-customer MER: –8.45%

- New-customer CAC: +19.56%

So the "typical" business is growing revenue but paying more for every new customer, with new-customer revenue slightly negative on the year.

Now look at the revenue-based size cut for February:

$50M–$100M businesses (median YoY change, Feb 2026 vs. Feb 2025)

- Spend: +16.37%

- Revenue: +14.83%

- New-customer revenue: –7.46%

- MER: –5.78%

- New-customer MER: –17.65%

- New-customer CAC: +28.69%

$100M+ businesses (median YoY change, Feb 2026 vs. Feb 2025)

- Spend: +16.80%

- Revenue: +17.29%

- New-customer revenue: +2.49%

- MER: +7.40%

- New-customer MER: –6.45%

- New-customer CAC: +12.30%

Both cohorts are growing faster than the market on topline, but neither is escaping pressure on new-customer acquisition economics.

$50M–$100M: Growth With Tightening Economics

For $50M–$100M businesses, February looks like a continuation of the 2025 trade-off, with more pressure on acquisition economics than the headline numbers suggest.

Spend up 16.37% and revenue up 14.83% is strong. But new-customer revenue is down 7.46%, meaning existing customers are doing most of the work. New-customer MER is down 17.65% and new-customer CAC is up 28.69%, meaning each new buyer is substantially more expensive and less efficient to acquire than a year ago.

If you sit in this size band, February should be treated less as proof that the 2025 playbook still works and more as a signal to harden guardrails before the economics deteriorate further.

$100M+: Strong Topline, Tighter Acquisition

The $100M+ cohort tells a more mixed story than the blended numbers suggest.

Revenue outpacing spend and blended MER up 7.40% reflects the leverage of a large, loyal customer base. But new-customer MER is down 6.45% and new-customer CAC is up 12.30%, consistent with the same market dynamic squeezing the $50M–$100M band, just less severely. New-customer revenue is at least positive (+2.49%), which separates this group from smaller peers, but the direction is the same.

For operators above $100M, the takeaway is measured optimism. Your retained customer base is a real asset. But treat new-customer metrics as a genuine constraint, not a lagging indicator that will self-correct.

How February Compares to January 2026

January 2026 already showed an early split by company size in our monthly benchmarks.

$50M–$100M, January 2026 vs. Jan 2025 (median)

- Spend: +7.07%

- Revenue: +5.91%

- New-customer revenue: +2.33%

- MER: –3.89%

- New-customer MER: –10.24%

- New-customer CAC: +15.25%

$100M+, January 2026 vs. Jan 2025 (median)

- Spend: +8.09%

- Revenue: +16.04%

- New-customer revenue: +8.22%

- MER: +0.83%

- New-customer MER: –0.68%

- New-customer CAC: +4.69%

$50M–$100M businesses pushed much harder in February, with spend and revenue growth accelerating significantly, but new-customer revenue flipped negative and CAC remained elevated. $100M+ businesses saw blended MER improve substantially, but new-customer MER swung from positive to negative and CAC worsened. At both size bands, acquisition economics tightened from January to February.

What This Means for Q2 2026 Planning at $50M+

If you are in the $50M–$100M band, the priority is guardrails. New-customer MER down nearly 18% and CAC up nearly 29% is a warning level, not a target. Any channel or creative that isn't helping reverse negative new-customer revenue should be constrained or redirected toward LTV.

If you are in the $100M+ band, the priority is protecting what's working. Your repeat base is giving you blended efficiency that smaller businesses can't match, but new-customer acquisition is getting more expensive. Keep first-time MER and CAC as first-class KPIs in weekly reviews, and treat creative throughput as a genuine bottleneck at current spend levels.

A Calm Bias Heading Into Spring

From our 2025 review through February 2026, the story above $50M comes down to this: growth is available, but the new-customer acquisition environment is getting harder at every scale, and spending more doesn't automatically fix it.

The $50M–$100M band is most exposed, with new-customer revenue negative and CAC up nearly 30%. The $100M+ band has the better blended story, but new-customer metrics are heading in the same direction.

For Q2 2026, let economics dictate how hard you press. If you are under $100M, treat February as a ceiling on acceptable new-customer deterioration. If you are above $100M, treat February as a reminder that your repeat base is an asset worth protecting, not a reason to ease up on acquisition discipline.

UPT (Units per Transaction) Explained: How to Calculate and Improve Retail Performance

In retail, small increases in basket size can generate meaningful revenue gains without adding new traffic.

UPT, or Units per Transaction, refers to how many items customers purchase in each completed sale. This guide explains what UPT is, how to calculate upt accurately, how it differs from related metrics like average order value, and practical strategies to improve it in stores and online.

Treated correctly, UPT is a powerful and controllable operational lever.

What is UPT in Retail and Why Does It Matter

UPT, or Units per Transaction, measures how many items a customer purchases in a single transaction.

If 100 customers complete purchases and collectively buy 250 items, your UPT is 2.5. In simple terms, it tells you the average basket size in units, not dollars.

UPT is widely used across brick-and-mortar stores, e-commerce sites, and omnichannel retail environments:

- Store managers use it to evaluate associate performance and merchandising effectiveness.

- E-commerce teams use it to assess cross-sell, bundling, and cart optimization strategies.

- In omnichannel environments, UPT helps identify how buying behavior differs between in-store, online, and buy online, pick up in store.

Because it focuses on customers who already decided to buy, improving UPT can increase revenue without increasing traffic or acquisition costs. Instead of finding more shoppers, you help existing buyers purchase just one more item. Over time, those small increases compound into meaningful gains in retail performance metrics.

The Units Per Transaction Formula Explained

The formula for UPT is: UPT = Total Units Sold ÷ Total Transactions

If you sell 1,200 items across 400 completed purchases, your UPT is 3.0. Meaning that, on average, each transaction includes three items.

“Units” should be clearly defined. A unit typically means an individual sellable item (not a dollar amount). If a customer buys three shirts, that is three units. If you sell bundles or kits, you need a consistent rule. Some retailers count a bundle as one unit because it is sold as a single SKU. Others break it into its component items for internal analysis. The key is consistency.

A “transaction” refers to a completed purchase event. In-store, that means a finalized receipt. Online, it means a confirmed order. Returns complicate the picture: if an item is fully returned, most teams subtract that unit from total units sold in the reporting period. For partial refunds, ensure your system adjusts unit counts accurately.

Common mistakes include mixing gross and net units, failing to account for returns, or inconsistently treating bundles. Clear definitions and standardized reporting prevent inflated or misleading UPT figures.

How UPT Interacts with Other Retail Metrics

UPT does not operate in isolation. It influences, and is influenced by, several other core retail KPIs:

- UPT vs. Average Order Value (AOV): UPT measures how many items are in the basket. While AOV measures how many dollars are in the basket. A retailer can increase AOV by raising prices without changing UPT. Conversely, UPT can rise while AOV stays flat if customers add lower-priced items.

- UPT vs. Conversion Rate: Conversion rate reflects the percentage of visitors who make a purchase. UPT only applies after a purchase occurs. A store may have strong conversion but low UPT, meaning shoppers buy just one item. Optimizing both improves overall revenue efficiency.

- UPT vs. Average Selling Price (ASP): ASP measures the average price per item sold. If ASP drops due to discounting, UPT may rise as customers add more units. However, revenue or margin may not improve proportionally.

Promotions, bundles, and threshold incentives often increase UPT. Price increases may reduce UPT if customers consolidate purchases.

If higher UPT is driven by heavy discounting or low-margin add-ons, gross margin per transaction may decline. Sustainable improvement requires balancing basket size with pricing discipline and margin performance.

How to Increase Units Per Transaction in Stores

Improving UPT in physical retail is largely about influencing behavior at the point of purchase through training, merchandising, and smart incentive design.

Associate Training And Cross-Sell Techniques

Store associates play a direct role in basket size. Training teams to suggest complementary products, ask open-ended questions, and make relevant recommendations can meaningfully increase units per transaction. The goal is not scripted upselling, but helpful guidance that enhances the customer experience.

Product Adjacency And Merchandising Layout

Physical layout shapes buying behavior. Placing complementary products near each other, such as accessories next to core items, increases the likelihood of incremental add-ons. End caps, checkout displays, and curated displays also create natural opportunities to expand baskets.

Bundles And Multi-Buy Promotions

Pre-packaged bundles simplify decision-making and encourage customers to purchase multiple items at once. Multi-buy offers, such as “three for two,” can lift UPT while maintaining perceived value.

Threshold promotions, such as “buy two, save,” can push shoppers to add one more item. However, guardrails are essential. Promotions should protect margin, avoid training customers to wait for discounts, and be measured carefully to ensure long-term profitability.

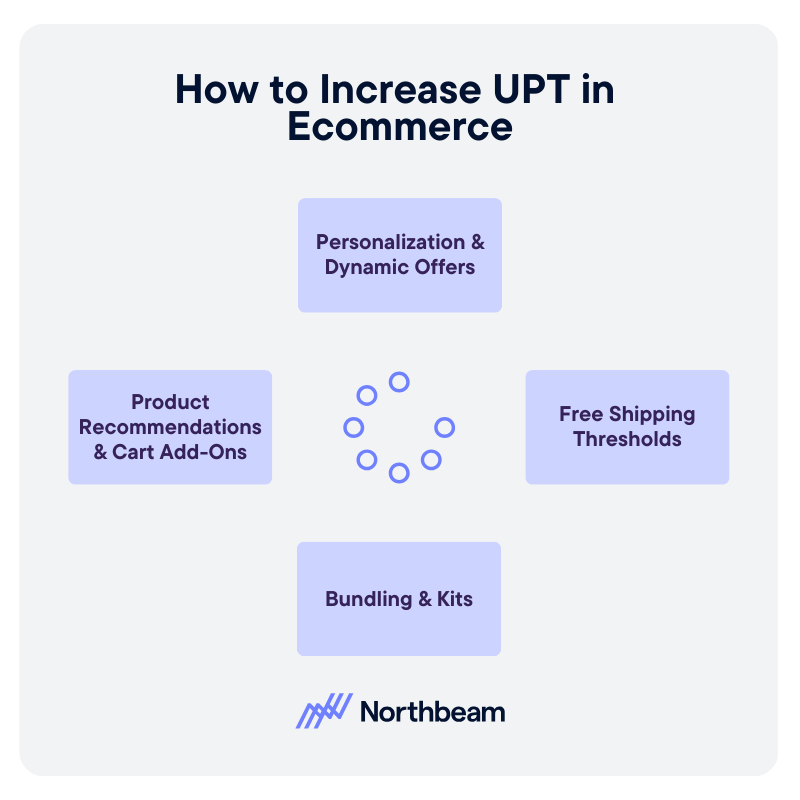

How to Increase Units Per Transaction in Ecommerce

In e-commerce, UPT growth depends on intelligent recommendations, thoughtful incentives, and a frictionless buying experience.

Product Recommendations And Cart Add-Ons

On-site recommendations are one of the most effective digital levers. “Frequently bought together,” “Complete the look,” and in-cart add-on suggestions surface complementary items at moments of high intent. The key is relevance. Irrelevant recommendations reduce trust and lower engagement.

Bundling And Kits

Digital storefronts make it easy to package related products into curated kits. Bundles reduce decision fatigue and increase perceived value while naturally increasing units per transaction. Clear pricing and visible savings strengthen performance.

Free Shipping Thresholds

Shipping thresholds encourage customers to add one more item to qualify for free delivery. When calibrated properly, this tactic lifts UPT without heavy discounting. The threshold should be based on average order value and margin targets.

Personalization And Dynamic Offers

Behavioral data enables personalized recommendations and dynamic cross-sell placements. Returning customers can see tailored suggestions based on browsing or purchase history, increasing basket expansion opportunities.

Too many pop-ups, irrelevant suggestions, or confusing layouts can backfire. UPT strategies should enhance the experience, not interrupt it. Clean design and seamless checkout preserve conversion while encouraging incremental units.

When Not to Push UPT

While increasing UPT can lift revenue, it is not always the right objective. Retail teams must weigh basket growth against margin, customer experience, and long-term loyalty.

Trade-Offs Between UPT And Margin

UPT often rises through discounts, multi-buy offers, or low-priced add-ons. If those incremental units carry thin margins, gross margin per transaction may decline even as basket size grows. A higher UPT that erodes profitability is not sustainable.

Impact On Returns And Customer Satisfaction

Aggressive upselling or forced bundling can increase post-purchase regret. Customers who feel nudged into unnecessary items are more likely to return products, which distorts UPT reporting and increases operational costs.

Long-Term Retention Considerations

Short-term basket expansion should not come at the expense of trust. Retailers that consistently prioritize helpful recommendations over pushy tactics tend to build stronger repeat purchase behavior.

If customers routinely remove recommended add-ons, abandon carts when bundles are required, or show rising return rates, your strategy may be too aggressive.

The most effective UPT strategies enhance value and convenience. When customers perceive recommendations as relevant and beneficial, basket size grows naturally without undermining brand equity.

UPT Measurement & Governance

UPT is most powerful when tracked alongside complementary metrics and governed with clear definitions and discipline.

KPIs To Track Alongside UPT

UPT should never be reviewed in isolation. Pair it with:

- Average Order Value (AOV): Ensures basket size growth translates into revenue.

- Gross Margin Per Transaction: Confirms incremental units are profitable.

- Conversion Rate: Identifies whether basket expansion efforts harm purchase likelihood.

- Return Rate: Flags whether added units lead to post-purchase regret.

- Revenue Per Visitor: Connects traffic, conversion, price, and UPT into one efficiency metric.

Together, these metrics show whether UPT growth is healthy or masking underlying issues.

Diagnostic Checks

Regular analysis helps isolate what is driving change:

- UPT by store, channel, and category

- UPT before and after promotions

- UPT trends across customer segments

Segmenting results prevents broad conclusions based on isolated wins.

Governance Considerations

Strong governance protects data integrity and margin:

- Maintain consistent unit definitions across channels

- Establish a clear reporting cadence

- Implement promotion approval guardrails

Clear ownership and standardized reporting ensure UPT becomes a strategic lever, not a vanity metric.

UPT Implementation Plan

Improving UPT requires structured execution, not isolated tactics. A phased approach ensures sustainable results.

Phase 1: Establish Baseline UPT

Begin by calculating current UPT across stores, channels, and key categories. Break results down by time period and customer segment to identify variability. This baseline creates benchmarks and highlights where performance is strongest or weakest.

Phase 2: Identify High-Impact Opportunities

Analyze where incremental gains are most realistic. For stores, this may include associate training or merchandising adjustments. For e-commerce, it may involve cart recommendations or free shipping thresholds. Prioritize initiatives based on potential lift, margin impact, and ease of execution.

Phase 3: Test And Measure Initiatives

Pilot changes in controlled environments. Test new cross-sell scripts in select stores or adjust recommendation placements on a subset of traffic. Measure UPT alongside AOV, margin per transaction, conversion rate, and return rate to ensure improvements are balanced.

Phase 4: Scale And Standardize

If results are positive and sustainable, roll out initiatives more broadly. Document best practices, align incentives, and maintain consistent reporting. Continuous monitoring ensures UPT growth remains profitable and aligned with brand strategy.

Turning Basket Size Into Sustainable Growth

UPT measures basket size and directly influences retail revenue efficiency. When customers add even one more item per transaction, the impact compounds across stores, channels, and time.

Accurate calculation requires consistent definitions of units and transactions. Without disciplined measurement, UPT can easily be overstated or misunderstood.

Sustainable UPT growth also depends on thoughtful merchandising, effective associate training, and seamless experience design. It works best when optimized alongside margin, conversion rate, and retention, ensuring that basket expansion strengthens profitability and long-term customer trust rather than eroding it.

Data Mapping Demystified: How to Connect and Visualize Your Data Sources

Most data problems do not begin in dashboards, but in the logic that connects one system to another.

Data mapping is critical because it defines how fields align, how definitions are interpreted, and whether numbers can be trusted across tools. When mappings are unclear or inconsistent, even the most sophisticated reporting becomes unreliable.

In this guide, we will explain what data mapping is and why it underpins accurate measurement. We’ll share practical data mapping examples for marketing data and outline a structured approach to implementing and maintaining it over time.

The goal is for you to be able to treat data mapping as a repeatable discipline that keeps your data aligned as your systems, tools, and teams evolve.

What Data Mapping Is And Why It Matters

Data mapping is the process of defining how fields from one system connect to fields in another. It answers practical questions like: Which source field populates this destination field? What format should it be in? Should it be transformed, normalized, or combined with other values?

In simple terms, data mapping creates the blueprint that allows systems to agree on what data means and how it moves.

Data mapping is not the same as ETL (Extract, Transform, Load) or reporting.

- ETL moves and transforms data.

- Reporting visualizes it.

- Data mapping sits upstream of both, defining the logic that makes those processes reliable.

If the mapping is wrong, the pipeline may run perfectly and the dashboard may look polished, but the numbers will still be misleading.

And mapping errors do cascade. A mismatched identifier can break attribution; an inconsistent definition of revenue can distort performance reporting; a missing normalization rule can inflate counts across systems.

When mapping is ignored early, downstream trust erodes, and teams spend more time debugging than deciding.

Data Mapping Best Practices and Examples

A reliable data mapping process starts with structure and clarity. Each component builds on the next, ensuring that data moves accurately, consistently, and in a way that supports downstream reporting and decision-making.

Source Systems and Ownership

Every mapping begins with clearly defined source systems. This includes marketing platforms, CRM, product databases, finance tools, and any system contributing data.

Just as important is ownership. Each source should have a responsible team or individual who understands how the data is generated, maintained, and changed. Without ownership, inconsistencies and silent schema changes go unnoticed.

Fields, Formats, and Data Types

Mapping requires field-level precision. Teams must define exact field names, formats, and data types. Is a date stored as a timestamp or string? Is revenue recorded in cents or dollars? Small mismatches in format or type can create large downstream discrepancies.

Transformation and Normalization Rules

Not all data can be copied directly from source to destination. Transformation rules define how values are cleaned, standardized, combined, or filtered. Normalization ensures consistency across systems, such as aligning country codes, campaign naming conventions, or currency formats.

Destination Schema and Definitions

The destination schema defines how data should look once integrated. Clear definitions for metrics, dimensions, and relationships prevent ambiguity. A shared understanding of what each field represents reduces reporting disputes later.

Documentation and Version Control

Data mappings should be documented and treated as living artifacts. Version control ensures changes are tracked, reviewed, and communicated, preventing unexpected breaks in reporting.

How to Visualize Data Mappings Clearly

Clear visualization turns data mapping from a technical artifact into a shared reference. The right format helps teams understand how data flows, where transformations occur, and how systems connect.

Here are a few best practices to keep in mind:

How to Create a Data Mapping Diagram: Tables, Flowcharts, Entity Relationships

Different visualization types serve different purposes:

- Tabular mapping is ideal for field-level detail, showing source fields, destination fields, data types, and transformation rules in a structured format.

- Flowcharts help illustrate how data moves between systems, making dependencies and handoffs visible.

- Entity relationship diagrams clarify how tables connect through keys and identifiers, which is especially useful in warehouse environments.

When to Use Visual vs Tabular Formats

Tables are best for precision and documentation, while diagrams are better for communication and alignment. Early planning conversations often benefit from visual flow diagrams, while implementation requires detailed mapping tables. Mature teams typically maintain both.

Keeping Mappings Readable as Systems Scale

As data integration mapping expands, mappings can become dense and difficult to interpret. Group related fields, separate logical domains, and avoid overcrowded diagrams. Modular documentation keeps complexity manageable.

Naming Conventions and Annotations

Consistent naming conventions reduce ambiguity. Annotations should explain transformations, exceptions, and assumptions. Clear labeling prevents future confusion when systems evolve.

Making Mappings Usable for Non-Technical Teams

Visualization should not exclude business stakeholders. Simplified diagrams, plain-language definitions, and contextual notes help non-technical teams understand how data supports reporting and decisions.

Common Data Mapping Challenges and How to Solve Them

Even well-designed mappings can break down over time. Most failures are not technical at their core; they stem from unclear definitions, shifting systems, or over-engineered logic.

Inconsistent Definitions Across Teams

Problem:

- Marketing defines revenue one way. Finance defines it another. Product tracks users differently than CRM tracks contacts.

- When teams operate with conflicting definitions, mapped fields may technically connect, but the meaning behind them diverges.

- This creates reporting discrepancies and ongoing reconciliation debates.

Solution:

- Establish standardized definitions and document them in a shared field dictionary.

- Align stakeholders before implementation, not after discrepancies appear.

- Governance reviews should include semantic validation, not just technical checks.

Missing or Unreliable Identifiers

Problem:

- Mappings depend on stable keys.

- If identifiers such as user IDs, order IDs, or campaign names are missing, inconsistent, or overwritten, joins fail and attribution breaks.

Solution:

- Prioritize durable identifiers early.

- Where gaps exist, implement fallback logic and enforce naming conventions.

- Audit identifier completeness regularly to prevent silent data fragmentation.

Schema Drift and Tool Changes

Problem:

- Vendors update APIs, fields are renamed, and new properties are added.

- Without monitoring, mappings degrade quietly, leading to incomplete or incorrect data downstream.

Solution:

- Implement schema change alerts and periodic mapping reviews.

- Treat integrations as living systems that require maintenance, not static infrastructure.

Over- or Under-Transformation

Problem:

- Too little transformation leaves inconsistencies unresolved.

- Too much transformation obscures source truth and complicates debugging.

Solution

- Apply only the transformations required for downstream use cases.

- Preserve raw data where possible, and document every rule clearly.

Data Mapping KPIs to Measure

Strong data mapping does not just improve integration accuracy, it also improves measurable operational outcomes. When mappings are well designed and actively maintained, teams spend less time debugging and more time making decisions.

Core KPIs influenced by effective data mapping include:

- Data completeness and freshness: Are expected fields populated, and are datasets updating on schedule?

- Error and reconciliation rates: How often do reports require manual correction or adjustment?

- Reporting consistency across systems: Do marketing, finance, and product dashboards align on shared metrics?

- Time-to-diagnosis for data issues: How quickly can teams trace discrepancies back to a specific field or transformation rule?

Monitoring these indicators helps detect mapping weaknesses early. Beyond KPIs, teams should implement regular diagnostic checks, such as:

- Field-level reconciliation samples to confirm values match across source and destination systems.

- Schema change impact reviews when APIs or tools update.

- Downstream report variance checks to identify unexpected swings caused by structural changes.

Mapping quality rarely fails loudly. Usually, it degrades quietly. Proactive measurement ensures small inconsistencies do not evolve into systemic reporting distrust.

Data Mapping Governance Considerations

Data mapping is not a one-time technical task; it requires ongoing governance to remain reliable as systems evolve and teams grow. Without structure and accountability, even well-designed mappings degrade over time.

Governance considerations should include:

Clear Ownership Per Data Domain

Every data source and destination should have a defined owner responsible for accuracy, changes, and documentation. Ownership ensures someone is accountable when discrepancies arise and prevents silent updates from breaking integrations.

Change Approval and Documentation Standards

Schema changes, new fields, and transformation updates should follow a documented review process. Version control and change logs help teams understand what changed, why it changed, and how it affects downstream reporting.

Regular Audits and Refresh Cycles

Periodic audits validate that mappings still align with business definitions and system configurations. Refresh cycles allow teams to clean up deprecated fields, adjust logic, and ensure the mapping framework continues to support evolving reporting needs.

Governance transforms mapping from a fragile setup into durable infrastructure.

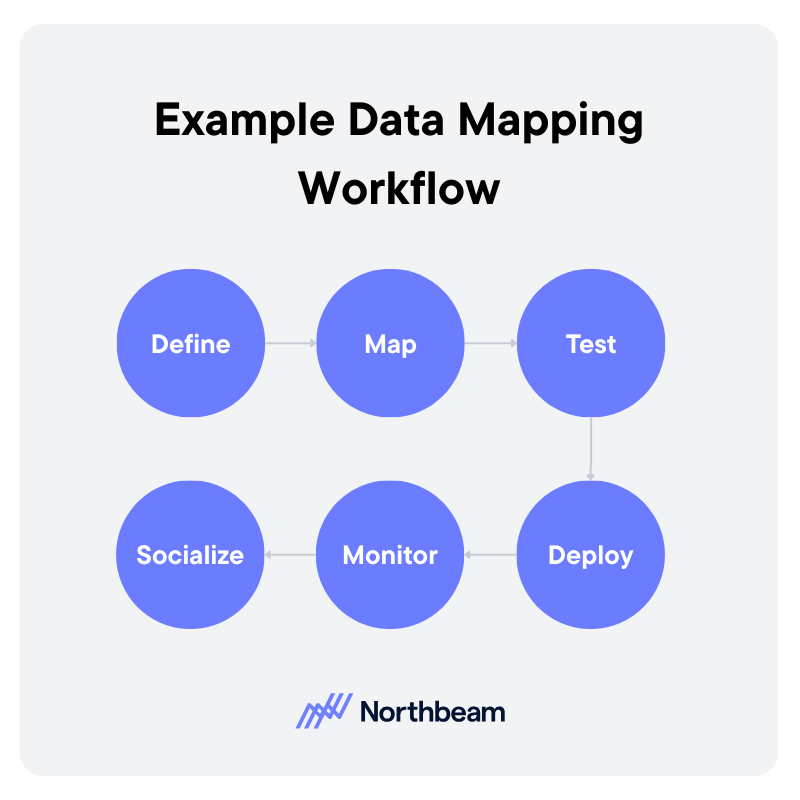

Example Data Mapping Workflow

A strong data mapping workflow is iterative and collaborative. It moves from definition to deployment, then continues through monitoring and refinement.

1. Define

Start by clarifying the use case and downstream requirements. What reports, dashboards, or models will depend on this mapping?

Identify source systems, required fields, definitions, and ownership. Clear scope prevents unnecessary transformations and keeps the mapping aligned with business needs.

2. Map

Document how each source field connects to the destination schema. Define transformation rules, normalization logic, and key relationships.

This step should produce a structured mapping artifact, such as a field-level table or diagram, that can be reviewed by stakeholders.

3. Test

Validate mappings before full deployment. Run reconciliation checks, confirm identifier integrity, and compare sample records across systems. Testing ensures that technical accuracy aligns with business definitions.

4. Deploy

Move the mapping into production pipelines or sync jobs. Ensure version control and documentation are updated to reflect the deployed configuration.

5. Monitor

After deployment, monitor data freshness, completeness, and report consistency. Investigate anomalies quickly to prevent silent degradation.

6. Socialize

Effective mapping requires coordination across analytics, engineering, operations, and business teams. Shared visibility and structured review cycles reduce friction and build trust in the resulting data.

From Integration to Insight

Data mapping tools and workflows determine whether systems align or quietly contradict each other. When mappings are thoughtfully designed and clearly documented, data moves with context and consistency instead of ambiguity.

Visual examples and structured artifacts make the logic understandable across technical and non-technical teams. Just as important, governance keeps mappings from degrading over time. Ownership, reviews, and validation routines ensure small changes do not turn into systemic reporting errors.

Strong data mapping is not just an integration task, but the very foundation for trustworthy measurement, reliable attribution, and confident decision-making.

Product

RESOURCES

Support

Legal

Follow us

.svg)