This article, our associated whitepaper, and the webinar I hosted, are based on Northbeam’s internal proprietary Clicks-Only data.

For DTC brands, Cyber Week 2025 wasn’t just “another record year.” It was a clear signal that peak season is now a strategy game, not a “spend big and hope for the best” game.

Across Northbeam’s customer base, we saw ad spend rise by just over 9% year over year, while revenue grew more than 13%, lifting MER even as first‑time CAC climbed about 8%. In other words: shoppers are still willing to buy, but they’re a lot more selective about when and how they convert.

This blog is a high‑level walkthrough of what we saw across thousands of DTC brands during Cyber Week 2025, and how the best teams are already adjusting their playbooks for 2026.

If you want the full channel‑by‑channel, industry, and company‑size breakdowns, grab the report this blog is based on:

Get the full data set: Download the BFCM 2025: The Report whitepaper for all charts, daily breakdowns, and industry cuts.

1. The window keeps widening: seed early, harvest late

Long gone are the days of lining up outside a big‑box retailer at midnight. The in‑store moment may have faded, but the online punch of Black Friday/Cyber Monday is absolutely still there, it just starts earlier and stretches longer.

When we looked at the 21‑day run‑up to Cyber Week (Nov 4–24), a few things stood out:

- Brands increased spend in the lead‑up; roughly mid‑single digits overall.

- Revenue in that same period grew a bit faster than spend.

- First‑time CAC jumped sharply, into the mid‑teens percentage‑wise.

Put simply, advertisers were priming the pump. They were willing to pay more to get in front of new customers before the sale, knowing that a meaningful chunk of that demand would only convert once the “real” offers went live.

That’s conversion lag in practice:

Dollars spent early in November convert during the sale itself, sometimes days or even weeks later.

If you only look at 1‑day click ROAS in‑platform, this early‑month spend can look terrible. When you look at it through a multi‑touch, cross‑channel lens, it suddenly becomes clear that your “expensive” pre‑BFCM dollars are actually doing a lot of the heavy lifting for peak week performance.

In the full report: we break down the Nov 4–24 period in more detail and show exactly how spend, revenue, MER, and first‑time CAC moved during those three weeks.

Watch the full webinar I hosted right here!

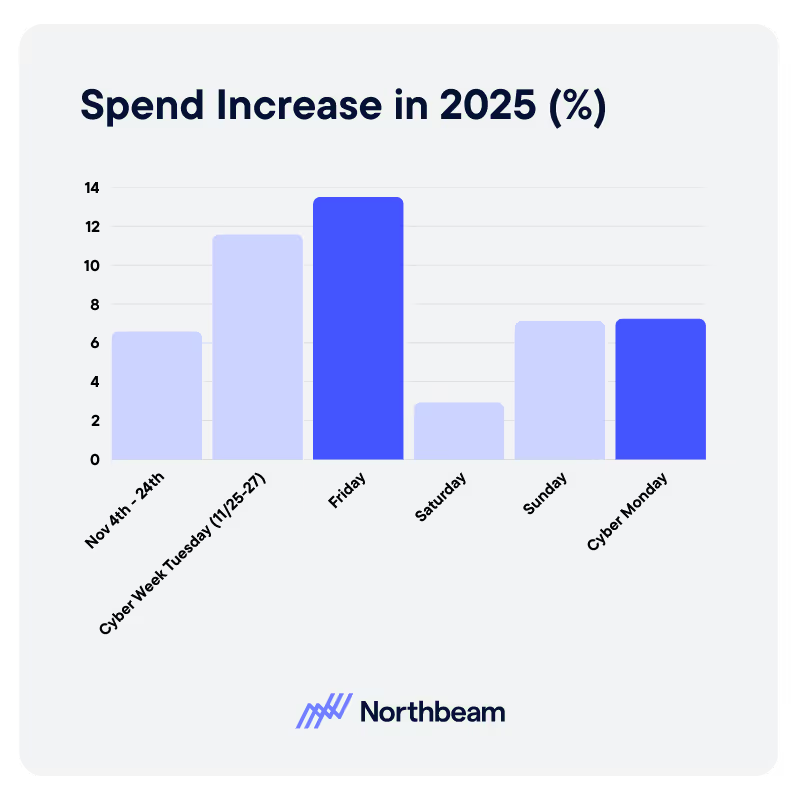

2. Cyber Week is a week‑long arc, not a single spike

From a distance, Cyber Week still looks like what you’d expect: spend ramps into Black Friday, stays elevated through Cyber Monday, then cools off. But when you zoom in day‑by‑day, the pattern is a lot more instructive.

Here’s the simplified version of what we saw:

- Tue–Thu (pre–Black Friday)

Brands ramped into the peak. Spend and revenue both moved up double‑digits vs. last year, MER improved modestly, and CAC started to climb as consumers browsed and waited. - Black Friday

Still the single biggest spend day of the week, but also the point where efficiency compressed the most. MER dipped relative to 2024 while CAC jumped by the mid‑teens as auctions got crowded and everyone piled in at once. - Saturday & Sunday

Many brands pulled back on spend on Saturday, and MER actually rebounded as the most motivated shoppers kept converting. By Sunday, both spend and revenue started to pick up again heading into Monday. - Cyber Monday

Spend re‑accelerated and efficiency improved vs. Black Friday, MER climbed, and CAC rose more modestly. This is the “I’ve been browsing all weekend and I’m finally pulling the trigger” behavior we heard anecdotally across accounts.

This is why we’re pushing clients to stop thinking in terms of “What’s my Black Friday budget?” and start thinking in terms of “What’s my Cyber Week arc?”

Some practical implications:

- You don’t need to front‑load 100% of your aggression into Friday. If you’re not seeing the results you expected, there’s a strong case for shifting some budget into Sunday/Monday next year, where competition can be slightly softer and intent is still high.

- When you evaluate performance, judge the week as a system, not as isolated days. A “weak” Thursday on a click‑only view might be exactly what you need to make Monday a record day.

3. Meta and Google still own the spine, but diversification is real

Despite all the noise about new platforms, Meta and Google are still the foundation of DTC performance marketing during Cyber Week.

Across our dataset:

- Together, Meta and Google represented roughly 80% of Cyber Week digital ad spend.

- Both platforms delivered strong revenue growth year over year and improvements (or stability) in short‑window ROAS, even as overall auctions remained competitive.

In other words: if you’re trying to build a BFCM media plan without Meta and Google as your budget spine, you’re swimming upstream.

That said, we did see meaningful wallet‑share movement elsewhere:

- TikTok: Brands significantly increased spend here, and revenue kept pace, especially for those willing to lean into video‑heavy prospecting and measure impact with Clicks + Deterministic Views (C+DV) instead of click‑only.

- Pinterest: Also saw solid budget growth. Performance was more mixed across accounts, but for visual, giftable categories, Pinterest remained a strong discovery and conversion assist channel.

- YouTube: Interestingly, we saw a slight decline in wallet share but much stronger revenue growth and ROAS among brands that stuck with it — alongside significantly cheaper CPMs. To us, that’s a classic sign of a channel that looks “meh” in last‑click, but quietly delivers revenue when you look at it through a multi‑touch lens.

The core takeaway:

Use emerging channels to diversify reach, not to “replace” Meta/Google.

Your job is to build a spine (Meta + Google), then layer in TikTok, Pinterest, YouTube, Snap, etc. in a way that actually adds incremental lift rather than just cannibalizing what you already have.

In the full report: we show detailed wallet share shifts, CPM/ROAS changes by platform, and a simple set of “rules of thumb” for how much budget most brands are safely putting into each non‑core channel today.

4. Size and category dictated who actually “won” Cyber Week

On aggregate, Cyber Week looks great. Under the hood, performance diverged sharply by company size and industry.

By company size

When we segmented brands by annual revenue, three different stories emerged:

- Large brands (>$100M)

- Spend up high single digits.

- Revenue up mid‑teens.

- MER up meaningfully, with only a small CAC increase.

- These teams tended to have their BFCM strategy dialed in — from promo structure to channel mix to upper‑funnel measurement.

- Mid‑market brands ($10M–$100M)

- Biggest increase in investment.

- The sharpest spike in CAC.

- MER roughly flat year over year.

- Growth was there, but it often came without efficiency gains. These are the brands that felt the most pressure from auction dynamics.

- Smaller brands (<$10M)

- More cautious on spend.

- Modest revenue lift.

- Small MER improvements, but less ability to simply “buy their way” into the peak.

By industry

We also saw clear category‑level winners and laggards:

- Strong performers:

- Beauty & Personal Care — grew spend and revenue, while actually improving first‑time CAC, making it one of the standout categories this year.

- Fashion & Accessories — consumers rewarded increased investment with outsized revenue growth; still a core Q4 gifting engine.

- Home & Furniture — solid returns suggest that considered, higher‑ticket purchases still respond well to strong seasonal offers.

- Sporting Goods & Fitness — brands that pulled back spend actually improved unit economics significantly, creating room to re‑invest smarter in 2026.

- Slower performers:

- Food & Beverage — advertisers pulled back, which helped stabilize MER, but rising CAC and modest revenue growth point to a tougher environment.

- Health & Wellness — arguably the most challenged category in the dataset: heavy investment, softer revenue, sharply higher CAC. Many brands tried to pull forward their usual Q1 “new year, new me” demand into Cyber Week — and it didn’t fully pay off.

The key message:

Your BFCM strategy has to be category‑specific. Elasticity, gifting dynamics, purchase frequency, and payback windows are wildly different by vertical — your benchmarks and budget ladders should be, too.

5. What to do now: four moves before you plan BFCM 2026

Coming out of Cyber Week, here’s how I’d recommend you operationalize these learnings.

1. Reset your benchmarks

Your “peak week” numbers are already out of date. Update:

- MER and CAC targets back to a more business‑as‑usual range.

- Channel‑level ROAS guardrails so your teams don’t keep optimizing to Black Friday conditions in January.

If you’re with Northbeam, this is a great time to align your Benchmarks/Stoplights with what “good” actually looks like post‑BFCM.

2. Use model comparison to understand what really drove 2025

If you only look at click‑only models, you’ll wildly underestimate:

- Upper‑funnel channels like TikTok, YouTube, Snapchat.

- Video‑heavy and creator/UGC campaigns.

- The early‑November “seed” campaigns that set up your Cyber Week harvest.

Swap between Clicks‑Only and Clicks + Deterministic Views (C+DV) in your reporting to see where net‑new demand actually came from in 2025, and use that to inform where you test harder in 2026.

3. Test smarter with MMM and incrementality

Media mix modeling (MMM) and incrementality testing have gone from “nice to have” to non‑negotiable:

- Use MMM to re‑forecast your 2026 channel mix based on what worked in 2025 — especially if you’re trying to push into new channels without blowing up CAC.

- Use incrementality tests to validate that your “growth channels” are actually adding incremental revenue, not just shifting credit around. Northbeam’s new incrementality solution also feeds those learnings back into MMM, so your model gets smarter, faster.

4. Lean back into creative and asset experimentation as CPMs cool

CPMs almost always cool off post‑BFCM, especially in Q1. That’s your window to:

- Launch new hooks, formats, and UGC concepts across your highest‑elasticity categories.

- Refresh offers and funnels for categories that struggled this year (looking at you, health & wellness and F&B) before you repeat 2025’s spend levels.

- Systematically log top‑performing creative from 2025 so you’re not reinventing the wheel next November.

Want the full data and all the charts?

This blog barely scratches the surface of what we saw in the data.

If you’re planning budgets for 2026 — or just trying to sanity‑check how your brand stacked up — I’d strongly recommend digging into the full whitepaper:

Download the full BFCM 2025: The Report to get:

- Day‑by‑day Cyber Week performance (Tue–Mon)

- Channel mix and wallet‑share shifts, including TikTok, Pinterest, YouTube, Snap, and more

- Performance by company size and industry, with detailed MER and CAC changes

- A deeper dive on how to use C+DV, MMM, and incrementality together

Cyber Week 2025 made one thing clear: the demand is still there — but the brands that win are the ones that plan, measure, and adapt smarter than everyone else.

.avif)

%25201.avif)

.avif)

.svg)