From a distance, 2025 looked like a clean win for ecommerce. Across Northbeam’s dataset, businesses increased ad spend and revenue, and the “growth is back” story finally felt true.

Up close, a little more nuance is required for the true read..

By vertical, 2025 was a year of trade‑offs: some categories grew fast but at the expense of MER and CAC, others protected economics and took slower topline, and a handful managed a more balanced path.

Using median results from our 2025 Year In Review whitepaper, here’s how eight major verticals actually performed, and what operators should do with that in 2026.

Download the full Northbeam 2025 data report.

Sporting Goods & Fitness: Aggressive Growth at a Cost

For Sporting Goods & Fitness, 2025 was a big year on revenue, but an expensive one.

At the median, businesses in this category increased spend by about +25% and grew revenue roughly +17%. That’s genuine expansion. But median MER fell by nearly 7%, first‑time MER dropped by more than 11%, and first‑time CAC climbed about +17% year over year.

In other words, every marginal customer cost significantly more and delivered less efficient revenue than in 2024, especially in the back half of the year where December was notably harsh for new‑customer economics.

2026 operator takeaway:

Treat Sporting Goods & Fitness as a category where early‑year is your acquisition window and the rest of the year should be managed accordingly. The data shows February through May as the most forgiving period for new‑customer growth. Use those months to build strong cohorts, then spend more of the back half defending MER and increasing LTV (bundles, upsells, replenishment) instead of forcing volume when CAC is structurally higher.

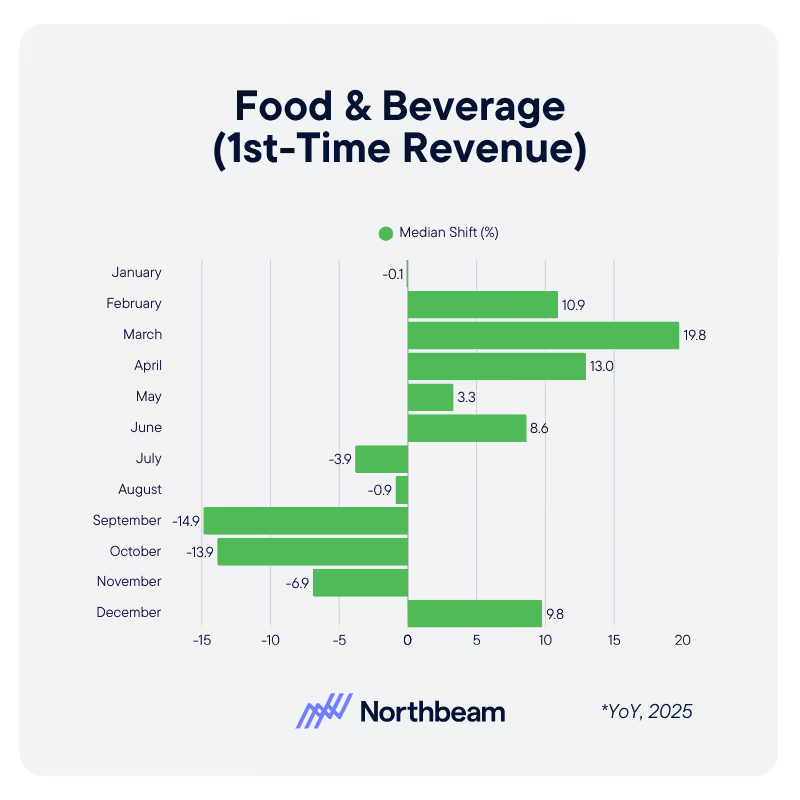

Food & Beverage: Growth that Leaned on LTV

Food & Beverage looks like a quiet success story on the surface. Median revenue grew a bit over +9% while median ad spend actually declined around –5%. That is a strong headline.

Underneath, the category was still under pressure. Median MER slipped by nearly 4%, first‑time MER by about 11%, and first‑time CAC increased more than 5%. In practical terms, businesses got better at squeezing revenue out of existing budgets and existing customers, but new customers were harder and more expensive to win.

2026 operator takeaway:

Plan as if higher acquisition costs are here to stay. That means:

- Setting clear CAC thresholds for prospecting.

- Designing acquisition and lifecycle together: subscription mechanics, post‑purchase flows, and thoughtful bundling that help you recoup weaker first‑time MER over time.

The businesses that treat LTV as part of their acquisition constraint, rather than an afterthought, will be the ones that can keep growing in this environment.

Home & Furniture: Timing as the Main Edge

Home & Furniture sits in a familiar position: high AOV, long consideration, and structurally higher CAC than many other categories. In 2025, median businesses grew spend by roughly +8.5% and revenue by about +9.0%, which means budgets and top‑line stayed fairly aligned.

The pressure showed up in how much it cost to create that revenue:

- Median MER declined about –2.6%.

- Median first‑time MER dropped around –7.5%.

- Median first‑time CAC increased close to +9.5%.

- Median first‑time revenue still grew about +6.7%.

So the sector did add new customers and revenue, but at a higher acquisition cost and tighter efficiency than the year before.

The nuance that matters is timing. The 2025 data highlights May and August as months where Home & Furniture businesses managed to grow revenue and hold comparatively better MER. Q4 produced strong revenue, but new‑customer economics in those weeks were noticeably weaker than in those spring and late‑summer windows.

2026 operator takeaway:

Think of the year as a sequence of deliberate acquisition campaigns rather than a constant push. Lean into proven intent peaks; move‑in seasons, refresh cycles, and the May/August windows the data calls out, and raise the bar for prospecting outside them. In this vertical, you win by being right on timing and payback, not by being “always on.”

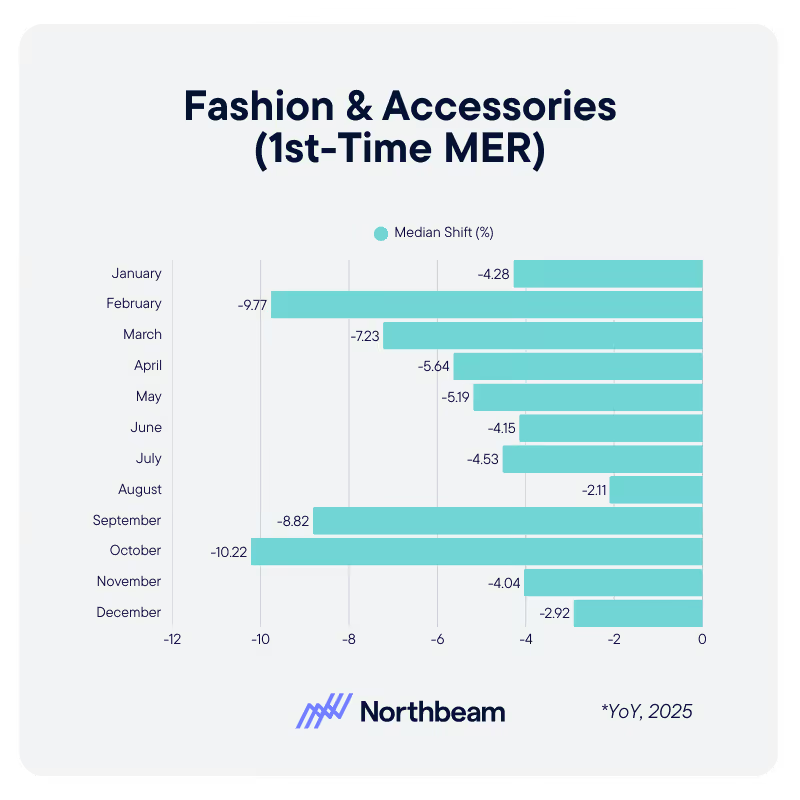

Fashion & Accessories: Growth Inside a Narrow Band

Fashion & Accessories did grow, but with very little margin for error. Median spend was up about +7%, median revenue roughly +6%. Meanwhile, median MER fell just under –2%, first‑time MER fell more than –5%, and first‑time CAC rose nearly +9%.

The monthly curves show a familiar pattern: a few “healthy” months, mainly late spring and early summer, where revenue and MER improved together, and long stretches where raising budgets simply meant paying more for the same or slightly worse revenue outcomes. Fashion could absolutely grow in 2025; it just could not grow indiscriminately.

2026 operator takeaway:

Treat Fashion as a tight‑corridor category. Use the whitepaper’s shape as a sanity check when you build your plan:

- Design scale around the months where your vertical historically supports both growth and MER.

- Cap CAC tightly in weaker periods.

- Use merchandising and bundling (for example, full‑look outfits or multi‑buy offers) to create AOV headroom that helps absorb higher CAC.

Beauty & Personal Care: Uneven Year, Mid‑Year Payoffs

Beauty & Personal Care had one of the more uneven journeys through 2025. At the median, spend and revenue both increased around +3–4%, but MER fell roughly –4%, first‑time MER about –8%, and first‑time CAC rose just over +4%.

Q1 stands out as particularly difficult: weaker revenue, compressed MER, and poor new‑customer economics created a sense that “growth feels bad.” Results improved later; mid‑year and in select Q4 periods, where businesses came in with well‑tested promos and creative instead of scrambling in‑season.

2026 operator takeaway:

Split the year in two:

- First half: a structured test phase for offers, bundles, and creative platforms that actually defend MER.

- Second half: execution—scale only what your own data shows is working.

In beauty, going into holiday with untested concepts is how you end up paying 2025‑style CAC for 2024‑style guesses.

Health & Wellness: Resolution Demand vs. Sustainability

Health & Wellness leaned hard into Q1 resolutions. At the median, spend increased about +9.4%, but revenue only around +4.3%. MER slipped roughly –1.5%, first‑time MER about –7%, and first‑time CAC climbed nearly +7.8%.

So yes, businesses won a lot of January and early‑year customers, but at worse efficiency than 2024. In the back half of the year, the category relied more on existing customers to carry growth as new‑customer economics stayed under pressure.

2026 operator takeaway:

For Health & Wellness, the critical question isn’t just how many people you bring in during January; it’s what those cohorts are worth over time. Use the 2025 shifts in first‑time CAC and first‑time MER as hard context when you:

- Define acceptable payback windows for your resolution campaigns.

- Design lifecycle programs, product pathways, and pricing that make those Q1 cohorts financially rational.

Only then decide how far you’re willing to push bids and budgets in the resolution spike.

Baby & Kids: When Always‑On Stops Working

Baby & Kids is where “spend more” was most clearly punished.

On averages, spend rose about +10%, but revenue only +2%, with average MER down roughly –7% and average CAC up +15%. Even at the median—where revenue grew a healthier +7.2% and MER improved about +2.4%—median CAC still increased around +4.2%.

Combine that with heavy seasonality and you get the real story: many businesses pushed budget into the wrong weeks at the wrong cost and paid for it in MER and CAC.

2026 operator takeaway:

Here, timing and cohort quality matter more than raw budget. Use the industry curves to identify:

- Which months and promo windows historically deliver both higher revenue and acceptable MER.

- Which high‑CAC pushes did not produce resilient cohorts or meaningful LTV.

Then build a 2026 plan that concentrates acquisition in those proven windows and runs lean everywhere else.

Technology: Big‑Business Aggression, Mixed Outcomes

Technology is the clearest example of aggressive scale in the report.

On averages, Tech businesses increased spend by about +38% and revenue by +28%, while average MER fell roughly –7% and average CAC jumped over +33%. At the median, things look milder: spend +1.3%, revenue +2.8%, MER +1.5%, but first‑time MER still down about –3% and first‑time CAC up roughly +13%.

The gap between average and median tells you what’s really happening: larger tech advertisers are driving the visible growth and are the ones most willing to accept painful CAC and MER trade‑offs. Smaller players are stuck in the same auction, with much less room for error.

2026 operator takeaway:

You cannot simply mirror the biggest budgets in your space. Use MMM and incrementality to determine:

- Where spend is truly creating net‑new demand.

- Where it’s just shifting conversions between channels or cannibalizing branded/organic.

Let the whitepaper’s Tech benchmarks define your upper limit on how much pain (MER decline and CAC increase) you’re willing to tolerate, not your default state.

How to Use These Takeaways In 2026

These industry breakdowns aren’t about bragging rights. They’re about understanding the shape of your category’s trade‑offs: how 2025 balanced revenue, MER, and CAC by vertical, and what that implies for 2026.

The key moves are:

- Benchmark locally, not globally. Compare your performance to businesses in your size band and vertical using the median stats, not to “ecommerce overall.”

- Set guardrails that reflect reality. Use the MER, first‑time MER, and CAC shifts above as the starting point for your 2026 floors and ceilings—not wishful thinking.

- Plan around your calendar shape. Build explicit scale windows and harvest windows using the months where your vertical actually supported efficient acquisition.

Every figure cited here, revenue, MER, and CAC changes by vertical, comes directly from Northbeam’s 2025 Year in Review. To download the full data set, click here.

.avif)

%25201.avif)

.avif)

.svg)