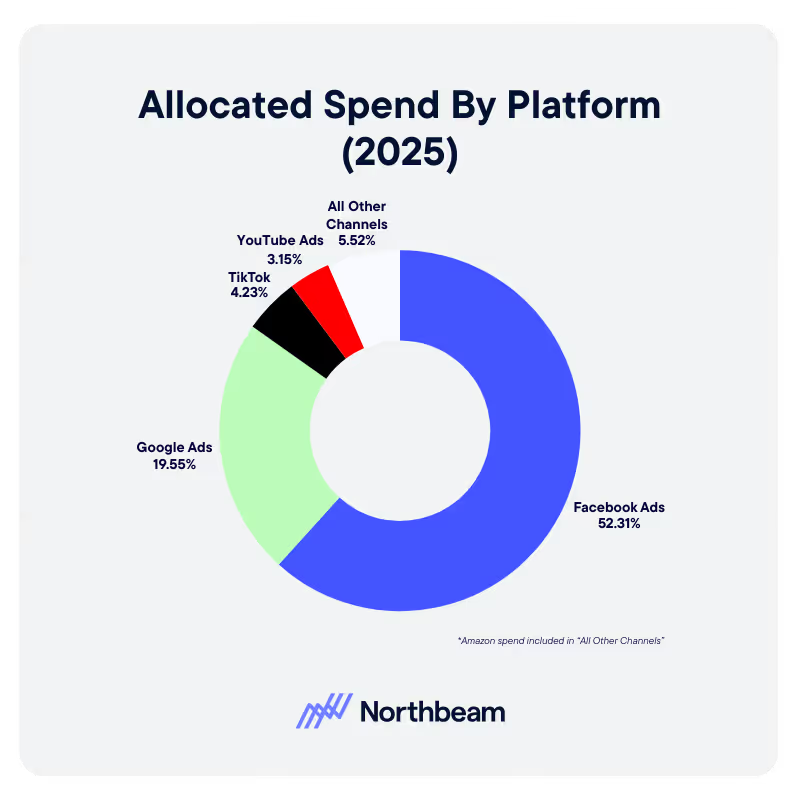

In 2025, ecommerce finally felt like growth mode again. Across Northbeam’s dataset, businesses increased ad spend and saw higher topline revenue year over year. On average, advertisers spent roughly 15% more on ads and generated a similar 14% lift in revenue, while the median business posted mid single digit gains on both lines.

The catch was what it cost to produce that growth. Marketing efficiency ratios (MER) softened and first time customer acquisition costs climbed. Median MER fell just over two percentage points, and median first time CAC was up nearly 9%, showing that incremental demand became more expensive to capture.

That is the core tension carrying into 2026: you could grow in 2025, but you probably did it with weaker unit economics. For some operators, that tradeoff was intentional and strategic. For others, it was a slow drift into paying more to stand still.

In 2026, the question is no longer whether growth is available. It is whether you can pursue it without eroding the economics that keep the business alive.

Download the full Northbeam 2025 data report.

This article reframes the key 2025 findings for a 2026 plan:

- What actually went wrong in 2025 from a unit economics standpoint

- How performance differed by company size and why that matters now

- The structural forces that pushed costs up even as revenue rose

- Concrete changes to make in 2026 if you want growth and durability

What “The Cost Of Growth” Really Means

Before digging into segments, it helps to reset the vocabulary you should be using to run 2026.

- MER (marketing efficiency ratio): Total revenue divided by total marketing spend. This is your blended, all in efficiency signal.

- First Time MER: First time customer revenue divided by total marketing spend. This isolates how efficiently you are acquiring new customers.

- CAC (customer acquisition cost): Total acquisition spend divided by the number of new customers.

On all three measures, 2025 was a step backward:

- Blended MER ticked down even as revenue rose.

- First time MER deteriorated faster than blended, which means acquisition was the main pressure point.

- First time CAC moved up meaningfully for the median business, and conversion rates declined, a sign that traffic quality worsened and fewer visits were truly net new.

So when we talk about “the cost of growth” in 2026, we are not being metaphorical. In 2025, businesses had to accept worse economics on each incremental dollar of new revenue.

This is the baseline to plan against now.

Who “Won” 2025 And What That Implies For 2026 By Size Band

The size breakdown makes the 2025 story much sharper and should directly shape your 2026 expectations.

Sub-$5M: Survival Mode To Discipline

Businesses under $5M in annual revenue had the roughest year:

- Median spend crept up only slightly, but median revenue actually declined.

- Both total and first time revenue fell, pointing to a cohort that could not deploy enough budget or convert it efficiently enough to keep up.

For these businesses, 2025 was less about “pay to grow” and more about pay more just to hang on. They prioritized cash preservation and margin protection rather than aggressive expansion.

In 2026, this segment should not pretend that a softer market will save them. The playbook is discipline: narrow guardrails on MER and CAC, simple attribution, and clear rules for when to pull back rather than chasing headline growth.

$5M–$20M: Comfortable But Fragile

In the $5M–$20M bands, the picture was more nuanced:

- Median spend and revenue both rose, with especially solid gains in the $10M–$20M tier.

- MER and CAC moved the wrong way, indicating that many businesses traded efficiency for modest growth.

This is the classic “comfortable but fragile” middle: enough budget to feel auction pressure and creative fatigue, but not enough operational scale to absorb mistakes or massively out-innovate the market.

In 2026, this tier must decide whether to behave like sub-$5M survivalists or $20M–$50M operators. Continuing to pay slightly more each quarter for slightly more revenue is how you end up boxed in by cash constraints and rising CAC.

$20M–$50M: Steady, Broad-Based Growth

The $20M–$50M cohort was one of the few genuine bright spots.

- Median stats showed spend and revenue moving up together, including first-time revenue.

- That suggests these businesses added volume without over relying on existing customers.

Even here, first time CAC and first time MER generally tightened. This group did not escape the 2025 acquisition environment. They simply managed it better than most by pairing scale with more disciplined guardrails.

In 2026, this tier is best positioned to compound if they protect their balance between topline and unit economics.

$50M+ And Enterprise: Deliberate Tradeoffs

At the top end, $50M+ businesses flipped from defensive to offensive:

- Median spend in the $50M–$100M and $100M+ bands climbed by roughly 18–23%, with revenue up in the mid teens.

- As we moved up the ladder, there was spend, more revenue, and higher first time CAC. The largest businesses were explicitly willing to trade efficiency for market share.

Upper mid and enterprise operators turned 2025 into a genuine step change year. Healthy fundamentals, well built out systems, and larger budgets helped them absorb the volatility that comes with algorithm driven advertising.

Why Unit Economics Deteriorated Even As Revenue Grew

Several overlapping forces drove the 2025 efficiency squeeze and will continue to matter in 2026.

1. Creative Fatigue And The Cost Of Staying In The Game

Across Meta, TikTok, Axon, YouTube, Pinterest, and Snap, there was a consistent relationship:

- As businesses moved into higher monthly spend bands, they launched dramatically more ads per month.

The platforms that drove growth in 2025 also demanded much higher creative velocity. For businesses that did not increase output at the same pace, creative fatigue showed up as rising CAC and sliding conversion.

That is another hidden cost of growth: systems, production, and internal operations that need to scale alongside budget and often do not.

2. Auction Pressure And More Low Intent Traffic

Across the dataset:

- First-time CAC increased.

- Blended and first time MER declined.

- Conversion rates fell.

That combination rarely happens by accident. It reflects two trends you should assume will still be in play this year:

- More businesses pushed back into growth mode, putting more budget into the same auctions and bidding up CPMs.

- A larger share of traffic was low intent or repeat. New visit percentage went down even as spend went up.

Net result: paying more per click to attract visitors who were less likely to convert and less likely to be truly net new. In 2026, ignoring new visit percentage is one of the fastest ways to quietly wreck your funnel.

3. Category Level “Growth At Any Cost”

Industry rollups showed how some verticals leaned into expensive growth:

- Sporting Goods and Fitness ramped spend and delivered some of the strongest median revenue gains, but median first time CAC jumped and first time MER fell, especially in the back half of the year.

- Technology businesses increased spend fastest of all, with big revenue gains and some of the steepest increases in CAC and declines in first time MER, particularly late in the year.

These are textbook examples of deliberately paying more per customer to secure category share. In 2026, treat these as upper bound scenarios when you model your own tolerance for CAC and MER deterioration.

For an industry-by-industry breakdown of the 2025 data, see my colleague CJ Hunter’s recent article.

4. Calendar Spikes That Loaded In Fragile Cohorts

Viewed month by month, 2025 looked less like a smooth climb and more like a series of cliffs:

- Median revenue growth was positive in most months.

- New customer revenue lagged or went negative in many of those same periods.

- Only a few months were true “pockets of efficient acquisition” where topline and first time performance improved together.

Q4 was especially revealing. Revenue spiked around peak promo moments, but in several categories first time MER and first time revenue deteriorated sharply in November and December, which implies a lot of holiday wins came from expensive, discount sensitive new cohorts.

In 2026, that pattern should inform when you are willing to pay up and what kind of cohorts you are willing to load during those windows.

How To Grow In 2026 Without Breaking Unit Economics

The final step is turning those 2025 lessons into a 2026 operating checklist.

1. Turn 2025 Numbers Into Explicit Guardrails

Set MER floors and CAC ceilings for 2026 that reflect what you learned last year:

- Decide how low MER can go across blended, first time, and returning revenue.

- Define CAC caps by product line, price point, and geography instead of relying on a single blended number. Different AOV bands live in very different CAC realities.

- Make these thresholds visible in daily and weekly views, not just in end of month recaps.

2. Separate Blended And New Customer Performance Everywhere

Returning customers repeatedly masked weaker acquisition economics in 2025. Fix that now:

- Report first time MER and first time CAC as first class KPIs.

- Investigate any period where revenue is growing but first time MER is slipping. Growth that rests on deteriorating new customer economics is not durable.

3. Benchmark By Size And Industry Cohort

Stop grading yourself against global averages:

- Compare your curves to businesses of similar revenue scale.

- Anchor your calendar and channel strategy to the shape of your category, whether that is resolution heavy Q1 in Health and Wellness or tight spring and summer efficiency windows in Fashion and Sporting Goods.

4. Scale Creative Systems Before Budgets

Treat creative capacity as a hard constraint:

- Commit to a minimum cadence of new concepts based on your spend band, calibrated to how many tests you can afford without crushing blended efficiency.

- Budget for the people and partners required to keep that cadence realistic.

- Use a measurement source of truth to decide which creative ideas actually move MER and CAC, not just in platform ROAS.

The 2026 Mindset Shift: From “Can We Grow” To “Can We Afford This Growth”

The 2025 data makes one thing clear: growth is no longer the scarce resource. Profitable growth is.

Businesses in the dataset proved they could grow spend and revenue. On average, they did exactly that. But the typical operator did it while accepting worse efficiency, more expensive new customers, and softer traffic quality.

So the real 2026 question is:

What does each additional dollar of growth actually cost you, and are you comfortable with that price

If 2025 was your “growth returned, but not on easy terms” year, let 2026 be the year you tighten guardrails, rebuild acquisition economics, and turn growth from something you buy into something your system can earn repeatably, at a price that keeps the business healthy enough to win your category over the long run.

.avif)

%25201.avif)

.avif)

.svg)