Profitability decisions often hinge on a simple question: what does it cost to produce one more unit?

Marginal cost measures the incremental cost of increasing output, making it a critical input for pricing, production planning, and growth decisions.

This guide explains the marginal cost formula, walks through practical examples, highlights common calculation mistakes, and shows how to use a marginal cost calculator.

Used correctly, marginal cost is not just an accounting concept, but a practical decision tool for evaluating scale, pricing, and operational efficiency.

What is marginal cost in business and why does It matter

Marginal cost measures the additional cost required to produce one more unit of output. Instead of looking at total spending across all production, marginal cost focuses on the incremental change that occurs when production increases.

Understanding marginal cost requires distinguishing between fixed costs and variable costs:

- Fixed costs, such as rent, salaries, or equipment leases, remain constant regardless of how many units are produced in the short term.

- Variable costs, including raw materials, packaging, and fulfillment expenses, rise as production increases.

Marginal cost reflects how these costs change when output expands.

Because it isolates incremental change, marginal cost is especially useful for operational decision-making. It helps businesses evaluate whether increasing production will improve profitability, determine pricing floors, and assess the financial impact of scaling output.

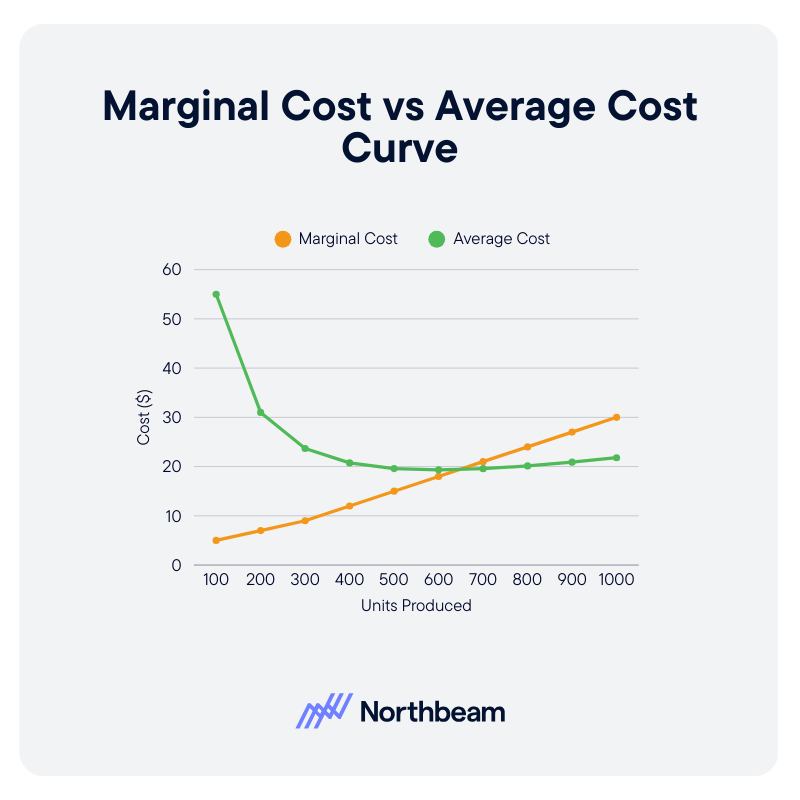

Marginal cost is often confused with average cost, but the two metrics answer different questions. Average cost divides total costs across all units produced, while marginal cost focuses specifically on the cost of producing the next unit.

Average costs decline over time as fixed costs are spread across more units. Marginal cost intersects average cost at the lowest point of the average cost curve, which is a standard economic relationship, before fixed costs start to increase to accommodate more production.

For pricing and production planning, marginal cost often provides the more actionable insight.

The marginal cost formula with examples

Here’s how to calculate marginal cost step by step:

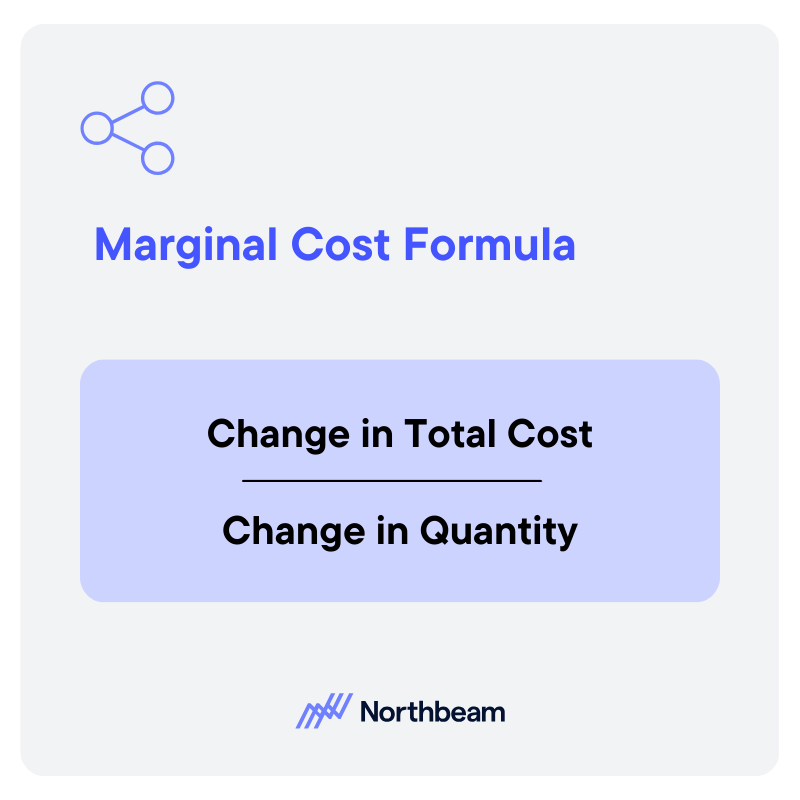

Marginal Cost = Change in Total Cost ÷ Change in Quantity

At its core, this formula measures how much additional cost is incurred when output increases.

Change in total cost means the difference between the total cost at one production level and the total cost at a higher production level.

This should include any costs that actually change as production rises, such as raw materials, direct labor, packaging, or shipping.

Fixed costs usually remain unchanged in the short term, though they can shift at certain production thresholds.

Change in quantity refers to the difference in the number of units produced between those two output levels. For example, if production rises from 1,000 units to 1,200 units, the change in quantity is 200.

In many business contexts, production changes are discrete, meaning output rises in whole units or batches. In economics, marginal cost may also be discussed more continuously, as the cost of producing one additional unit at any point on the cost curve.

For most business applications, though, the practical approach is to calculate it across a real change in output.

For example, if total cost rises from $10,000 to $11,200 when production increases from 1,000 to 1,200 units, marginal cost is $1,200 ÷ 200 = $6 per unit.

Marginal cost examples across different business contexts

Marginal cost behaves differently depending on the type of business and its cost structure. Looking at examples across industries helps illustrate how the concept applies in practice.

Manufacturing

In manufacturing, marginal cost typically reflects the additional materials, labor, and energy required to produce more units.

For example, a furniture manufacturer may spend $50 on wood, hardware, and labor to produce each additional chair once the factory is already operating.

In this case, the marginal cost of one more chair is roughly $50, assuming no major capacity changes.

SaaS/Digital products

For SaaS and digital products, marginal cost is often extremely low. Once the software platform is built, the cost of adding another user might be limited to incremental cloud infrastructure, customer support, or payment processing fees.

If those additional costs total $0.30 per user, then the marginal cost of serving one more customer is about thirty cents.

Ecommerce

In e-commerce, marginal cost typically includes product cost, packaging, and fulfillment expenses. If an online retailer pays $15 for inventory and $4 for shipping and packaging, the marginal cost of fulfilling an additional order might be around $19.

Cost structure considerations

Cost structure also influences how marginal cost behaves.

Businesses with high fixed costs, such as software platforms or factories, often see marginal costs decline as production scales. In contrast, low fixed-cost businesses with high variable inputs may see marginal costs remain relatively stable as output increases.

How to use a marginal cost calculator

A marginal cost calculator can help quickly estimate the incremental cost of increasing production. To use one correctly, you need two core inputs:

- Total cost before the production change

- Total cost after the change

You also need the corresponding output levels for each scenario.

For example, if producing 1,000 units costs $10,000 and producing 1,200 units costs $11,200, the calculator will determine the marginal cost by dividing the change in cost by the change in quantity.

While calculators simplify the process, it is still helpful to understand the manual formula behind them.

In spreadsheets, the same calculation can be implemented with a simple formula:

(New Total Cost – Previous Total Cost) / (New Quantity – Previous Quantity).

This allows teams to model multiple scenarios and update assumptions quickly.

Marginal cost calculators can also be used in reverse. By estimating the marginal cost of producing additional units, businesses can approximate break-even thresholds or evaluate whether scaling production will improve profitability.

However, calculator outputs should always be interpreted carefully. Marginal cost reflects a specific production change, not a universal cost per unit. Capacity limits, input price fluctuations, and operational constraints can all shift the result.

Marginal cost calculator

Use the calculator below to estimate the incremental cost of increasing production. Enter the total cost and output level before and after a production change to quickly compute the marginal cost per additional unit.

Marginal cost and pricing decisions

Marginal cost plays an important role in pricing strategy, but it should be used as a decision input, not the only pricing rule. Understanding how incremental costs interact with margins, demand, and competitive dynamics helps businesses set sustainable prices.

Pricing floors and marginal cost

Marginal cost often serves as a practical pricing floor. Pricing below marginal cost means each additional sale increases losses because the revenue generated does not cover the incremental cost of producing that unit.

In most cases, businesses aim to price above marginal cost so that each additional unit contributes to covering fixed costs and generating profit.

Contribution margin considerations

Pricing decisions should also consider contribution margin, which is the difference between price and marginal cost. A healthy contribution margin ensures that each sale contributes toward fixed costs such as salaries, infrastructure, or rent.

For example, if a product sells for $20 and the marginal cost is $8, the contribution margin is $12. This margin is what allows the business to recover fixed costs and eventually generate profit.

Short-term vs long-term trade-offs

In some cases, businesses may temporarily price close to marginal cost. This can happen during promotions, market entry, or efforts to increase utilization of existing capacity.

However, sustained pricing near marginal cost can be risky if it does not cover fixed costs over time.

Risks of misusing marginal cost

Marginal cost alone should not determine pricing strategy. Competitive dynamics, customer demand, and brand positioning all influence what customers are willing to pay.

Over-relying on marginal cost can lead to underpricing products and leaving potential revenue on the table.

Common marginal cost mistakes

Marginal cost is a useful decision tool, but it is easy to misuse if the underlying assumptions are misunderstood. Several common pitfalls can lead to inaccurate calculations or poor business decisions.

Ignoring step-fixed costs

Many costs appear fixed until production crosses a certain threshold. For example, a factory may operate with one supervisor up to a certain output level, but adding a second production shift requires hiring another supervisor.

These step-fixed costs can cause marginal cost to jump suddenly when capacity limits are reached.

If these thresholds are ignored, marginal cost estimates may look artificially low and lead to overly aggressive pricing or expansion decisions.

Confusing accounting costs with economic costs

Accounting records typically capture explicit expenses such as materials, labor, and overhead. However, economic costs may also include opportunity costs, such as alternative uses of labor, equipment, or production capacity.

Relying solely on accounting costs can underestimate the true cost of producing additional units, especially in constrained environments.

Using marginal cost without demand context

Marginal cost helps explain the cost side of a decision, but it says nothing about customer demand or willingness to pay. A product priced slightly above marginal cost may still fail if the market will not support the price.

Pricing decisions should therefore consider both marginal cost and expected revenue dynamics.

Over-optimizing for short-term efficiency

Focusing too narrowly on marginal cost can encourage decisions that maximize short-term efficiency but undermine long-term strategy. For example, cutting service quality or delaying maintenance might temporarily reduce marginal costs while creating larger costs later.

Practical guardrails

To avoid these pitfalls, businesses should track marginal cost alongside other metrics such as contribution margin, capacity utilization, and demand signals.

Regular sensitivity analysis and cross-team alignment between finance and operations also help ensure marginal cost calculations remain realistic and actionable.

Marginal cost implementation plan

Applying marginal cost analysis consistently requires a clear process across finance and operations. A phased implementation helps organizations move from rough estimates to reliable decision support.

1. Audit cost structure

Start by identifying how costs behave across the business. Finance teams should separate fixed costs from variable costs and document how expenses change as production increases.

This step often involves reviewing accounting systems, ERP data, and operational records to ensure cost categories are accurate and consistently defined.

2. Establish baseline marginal cost

Once costs are categorized, teams can calculate a baseline marginal cost using recent production data. This involves comparing total costs at two different output levels and applying the marginal cost formula.

Documenting this methodology ensures that future calculations use the same assumptions and time windows.

3. Integrate into pricing and planning

With a baseline in place, marginal cost can be incorporated into pricing strategy, capacity planning, and financial forecasting.

Leadership and finance teams can use the metric to define pricing guardrails, evaluate scaling decisions, and model how production changes affect profitability.

4. Ongoing monitoring and refinement

Marginal cost is not static. As input prices, production volumes, or operational processes change, the calculation must be updated. Regular monitoring helps ensure models remain accurate and reflect real operating conditions.

Marginal cost as a decision tool

Marginal cost measures the incremental cost of producing one additional unit of output. Calculating it accurately requires clear cost categorization and consistent tracking of production levels.

When applied correctly, marginal cost helps businesses understand how production changes affect profitability. It informs pricing floors, scaling decisions, and operational planning.

And used thoughtfully alongside metrics like contribution margin and capacity utilization, marginal cost becomes a practical tool for smarter financial and strategic decision-making.

.avif)

%25201.avif)

.avif)

.svg)